What Do You Need To Consider When Planning Retirement?

When is the best time to get serious about retirement planning? Some say it’s the 50’s. And guess what, it’s not all about you. It’s about your parent’s too. “It’s important to talk openly with your parents about their financial position and plans,” said Matthew Saneholtz, a certified financial planner with Tobias Financial Advisors. “Be sure your parents have an estate plan in place and long-term care coverage, or at least a picture of their final stages of life, because it might affect you,” he said. “If you know your parents don’t have the money to pay for care on their own, are you willing to use your own savings to help them? Will they rely on Medicaid? Will you take care of them in your own home? These are questions you need to think about, as they could become your dependents.”

Source: Your 50s Is the Time to Get Serious About Retirement Planning“.

Individual Retirement Arrangements (IRAs)

Roth IRAs

401(k) Plans

403(b) Plans

SIMPLE IRA Plans (Savings Incentive Match Plans for Employees)

SEP Plans (Simplified Employee Pension)

SARSEP Plans (Salary Reduction Simplified Employee Pension)

Payroll Deduction IRAs

Profit-Sharing Plans

Defined Benefit Plans

Money Purchase Plans

Employee Stock Ownership Plans (ESOPs)

Governmental Plans

457 Plans

409A Nonqualified Deferred Compensation Plans

Help with Choosing a Retirement Plan

We do more than just tax preparation. US-TaxLaws is your best source for professional tax preparation and/or financial consulting services that include:

Personal Tax Preparation Business Tax Preparation Partnership Tax Preparation

Corporate Tax Preparation Incorporation-Choice of Entity Business Support Services

Corporate Compliance Audit Representation Retirement Tax Planning Wills & Trusts, Estate Planning Bookkeeping Payroll

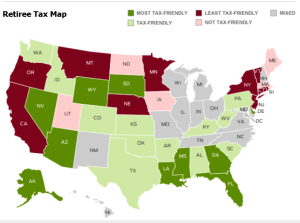

Methodology

Methodology In 2015, Various Tax Benefits Increase Due to Inflation Adjustments

In 2015, Various Tax Benefits Increase Due to Inflation Adjustments

IRS cost‑of‑living adjustments affect dollar limitations for pension plans and other retirement-related items for tax year 2014.

IRS cost‑of‑living adjustments affect dollar limitations for pension plans and other retirement-related items for tax year 2014.  Retirement is one of the big questions Boomers are facing and keep these thoughts in mind when planning.

Retirement is one of the big questions Boomers are facing and keep these thoughts in mind when planning.