Facebook, GE, Johnson & Johnson and other stocks that Baby Boomers love.

Facebook, GE, Johnson & Johnson and other stocks that Baby Boomers love.

If you are a Baby Boomer, and have investments in your retirement planning, you’ll enjoy this article. Forbes writer, Samantha Sharf, looks at the stocks that the different generations favor. “Johnson & Johnson JNJ -0.59% is the tenth most popular stock among Baby Boomers — the generation born between 1946 and 1964 — making up 0.9% of the average Boomer’s stock portfolio, according to TD Ameritrade. Two key facts make a strong case for why the healthcare giant ranks with this group but not their younger counterparts.

First fact: Boomers are turning 65 at a rate of about 10,00 per day. That trend is expected to continue until around 2030, according to Pew Research.

Second: Last year Fidelity Benefits Consulting estimated a 65-year-old couple will need an average of $220,000 to pay for medical expenses throughout retirement. That’s a lot.”

“The healthcare giant ranks 14th for Millennials’, the youngest adult generation, and 22nd for Gen Xers, the generation just behind Boomers. Johnson & Johnson, however, is even more popular with people over 70 making up 1.1% of a Senior’s portfolio on average.”

Stocks Baby Boomers Love Most:

Apple

General Electric

Microsoft

Facebook

Bank of America

Intel

AT&T

Exxon Mobil

Berkshire Hathaway

Johnson & Johnson

Read original article “Johnson & Johnson and the 9 other stocks Baby Boomers Love Most“.

We do more than just tax preparation. US-TaxLaws is your best source for professional tax preparation and/or financial consulting services that include:

Personal Tax Preparation Business Tax Preparation Partnership Tax Preparation

Corporate Tax Preparation Incorporation-Choice of Entity Business Support Services

Corporate Compliance Audit Representation Retirement Tax Planning Wills & Trusts, Estate Planning Bookkeeping Payroll

IRS Issues An Identity Theft Alert To Taxpayers

IRS Issues An Identity Theft Alert To Taxpayers

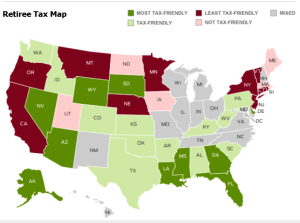

Methodology

Methodology

Seven significant new income tax law changes went into effect at the beginning of the year as a result of two pieces of legislation:

Seven significant new income tax law changes went into effect at the beginning of the year as a result of two pieces of legislation:

IF YOU WANT TO GET CREDIT FOR CHILD and DEPENDENT CARE, THE IRS NEEDS TO KNOW…

IF YOU WANT TO GET CREDIT FOR CHILD and DEPENDENT CARE, THE IRS NEEDS TO KNOW…  TAX MOVES TO MAKE BEFORE CHRISTMAS.

TAX MOVES TO MAKE BEFORE CHRISTMAS. Mid Year Tax Questions You Need To Ask Yourself

Mid Year Tax Questions You Need To Ask Yourself