New Standard Mileage Rates Just Announced by IRS ; Business Rate to Rise in 2015

New Standard Mileage Rates Just Announced by IRS ; Business Rate to Rise in 2015

WASHINGTON — The Internal Revenue Service today issued the 2015 optional standard mileage rates used to calculate the deductible costs of operating an automobile for business, charitable, medical or moving purposes.

Beginning on Jan. 1, 2015, the standard mileage rates for the use of a car, van, pickup or panel truck will be:

- 57.5 cents per mile for business miles driven, up from 56 cents in 2014

- 23 cents per mile driven for medical or moving purposes, down half a cent from 2014

- 14 cents per mile driven in service of charitable organizations

The standard mileage rate for business is based on an annual study of the fixed and variable costs of operating an automobile, including depreciation, insurance, repairs, tires, maintenance, gas and oil. The rate for medical and moving purposes is based on the variable costs, such as gas and oil. The charitable rate is set by law.

Taxpayers always have the option of claiming deductions based on the actual costs of using a vehicle rather than the standard mileage rates.

A taxpayer may not use the business standard mileage rate for a vehicle after claiming accelerated depreciation, including the Section 179 expense deduction, on that vehicle. Likewise, the standard rate is not available to fleet owners (more than four vehicles used simultaneously). Details on these and other special rules are in Revenue Procedure 2010-51, the instructions to Form 1040 and various online IRS publications including Publication 17, Your Federal Income Tax.

Besides the standard mileage rates, Notice 2014-79, posted today on IRS.gov, also includes the basis reduction amounts for those choosing the business standard mileage rate, as well as the maximum standard automobile cost that may be used in computing an allowance under a fixed and variable rate plan.

Notice 2014-79 provides the optional standard mileage rates for substantiating the amount of deductible expenses for using an automobile for business, moving, medical, or charitable purposes. For 2015, the standard mileage rates are 57.5 cents for business use of an automobile, 14 cents for use of an automobile as a charitable contribution, and 23 cents for use of an automobile as a medical or moving expense.

Notice 2014-79 also provides the amount a taxpayer must use in calculating reductions to basis for depreciation taken under the business standard mileage rate and the maximum standard automobile cost that a taxpayer may use in computing the allowance under a fixed and variable rate plan.

The rules for using the optional standard mileage rates to calculate the amount of a deductible business, moving, medical, or charitable expense are in Rev. Proc. 2010-51.

Notice 2014-79 will be in IRB IRB 2014-53, dated December 29, 2014.

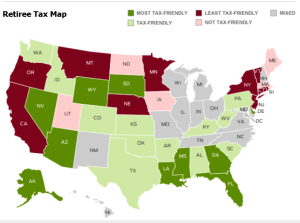

Want to know where is the best place to live in retirement?

Want to know where is the best place to live in retirement? Entity creation has a cost!

Entity creation has a cost! Special per diem rates for lodging, meals, and incidental expenses.

Special per diem rates for lodging, meals, and incidental expenses.